Monthly NewsletterJanuary 2025

Jan 1, 2025

Workers’ financial health has improved somewhat this year, as 401(k) participants increasingly credit their employers for helping to manage financial stress, a new study finds.

According to Charles Schwab’s 2024 401(k) Participant Study, 64% of workers say their employers have taken action to help them manage financial stress, compared to 52% who said the same last year.

When asked what their employer has done in the past year, if anything, that helped them manage their financial stress, increases to their salary and 401(k) match, along with flexible work arrangements, were cited by employee respondents as the most impactful actions that employers took.

In addition, more workers report feeling “very good” about their financial health (24%) compared to last year (20%). Overall, roughly 80% of workers say their current financial health is either “very good” or “pretty good.” That said, there’s still work to do, as many continue to feel stressed. About half of workers say their financial health has not changed, while one in five say it has worsened. GenZ (37%) and Millennials (35%) are more likely to say their financial health has improved, compared to Gen X (28%) and Boomers (21%).

“While the markets have generally performed well this year, inflation and economic conditions have continued to put pressure on workers’ finances at elevated levels,” noted Lee McAdoo, Managing Director of Schwab Retirement Plan Services. “In the face of external economic factors, employers are supporting their employees with a combination of direct financial assistance and accompanying resources to help them manage financial stress and overall well-being.”

Schwab’s survey was conducted by Logica Research between April 17 and May 3, 2024, among 1,000 U.S. 401(k) plan participants. Respondents were actively employed by companies with at least 25 employees, were 401(k) plan participants and were 21-70 years old. Additional details about the results can be found here.

The letters from Great Gray and its counsel, Covington & Burling LLP and Groom Law Group, are part of an effort to get a bill passed before the year is out that will allow CIT investing by nonprofit organizations ranging from schools to churches. The effort is also, in part, a response to a letter six investor advocacy groups sent to the committee earlier in November seeking to kill the proposal.

In that letter, six groups that included the Americans for Financial Reform and the Consumer Federation of America argued that CITs—which, unlike mutual funds, are not registered with the Securities and Exchange Commission—would expose 403(b) plan participants to investment risks. They argued that the bill would expose more investors to the risks of “illiquid, opaque, high-risk and often predatory private markets.”

The bill to allow 403(b)s to use CITs, S.5139, the Empowering Main Street in America Act, was introduced in September by Senator Tim Scott, R-South Carolina, the ranking member of the Senate Committee on Banking, Housing and Urban Affairs. That bill and one introduced in the House of Representatives are a continuation of the effort begun in the SECURE 2.0 Act of 2022, but not included in final legislation, to enable 403(b) plans to invest in instruments beyond the annuity contracts and mutual funds to which they are currently limited.

In its letter Great Gray Trust and its partners argued that CITs are regulated both by the Office of the Comptroller of the Currency and by the Employee Retirement Income Security Act, by nature of their use in DC plans.

“CITs often have lower fees and expenses than other pooled investment products like mutual funds and variable annuities,” Great Gray CEO Rob Barnett wrote in the letter. “At the same time, CITs offer enhanced investor protections because they are subject to a regulatory regime that is specifically designed for retirement plan investors. These advantages help explain why private sector retirement plans are increasingly selecting CITs over mutual funds and other investment products to help Americans grow their retirement savings.”

As of this year, CIT target-date funds “inched past” mutual fund TDFs by way of assets, according to data from Morningstar. Barnett referenced the consumer advocacy groups’ letter, countering the idea that CITs would harm retirement savers with the argument that CITs would expand access to lower-priced options.

“Passage of the CIT Bill will remove a disadvantage, not create one, by giving 403(b) plans access to CITs, which private sector 401(k) plans have today,” Barnett wrote. “Providing 403(b) plans with much needed access to lower-cost CIT investments could boost the retirement savings of non-profit employees by tens or even hundreds of thousands of dollars over the course of their careers.”

Barnett also made the case that CITs, which are subject to ERISA, would come with “stringent regulatory protections” for the non-ERISA 403(b) plan space. A 403(b) plan should be allowed to make its own choice between “a lower cost CIT that is subject to ERISA over a higher cost mutual fund that is not subject to ERISA,” he wrote.

Attorneys from Covington & Burling and Groom Law detailed how CITs are regulated and administered as bank trust products. Covington & Burling sent a letter to individual senators, while Groom Law focused on Scott, the ranking member of the Senate Banking Committee, and its chair, Senator Sherrod Brown, D-Ohio.

The specter of regulatory review of CITs has been raised multiple times by the current head of the Securities and Exchange Commission, Gary Gensler. But Gensler announced his resignation for January 20, 2025, to coincide with the inauguration of President-elect Donald Trump.

The current Congress will have a final chance to pass pending legislation in its December lame duck session before the new administration and Republican-majority Congress take over on January 3, 2025.

Goodbye 2024, Hello 2025!

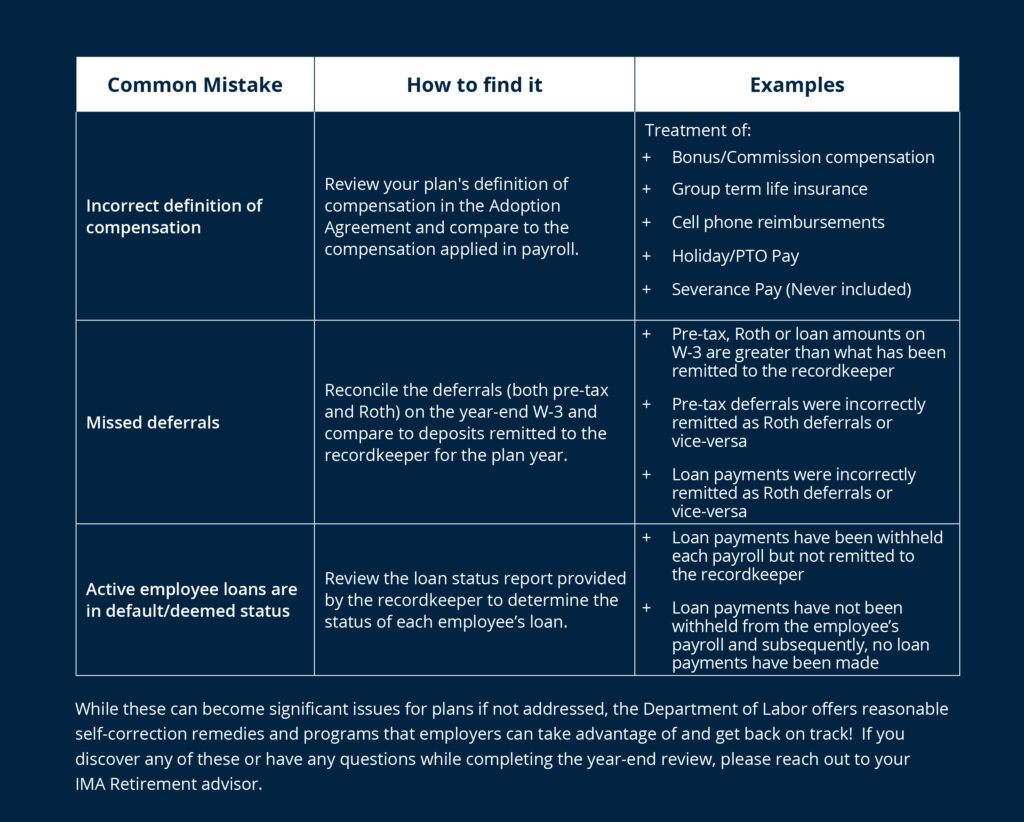

While the year comes to an end, the start of a new begins which can only mean one thing for HR directors and controllers alike – retirement year-end compliance census and business questionnaires. While not everyone’s favorite, it is a good time to do a check on the plan and determine if any common plan mistakes have occurred during the year and if caught, many times, easy corrections can be made to maintain the plan’s compliance status.

At IMA Retirement, we believe that our team’s dedication and expertise are the keys to serving the needs of our clients and their employees. This month, we’re thrilled to introduce you to John Alvarez, one of our Retirement Plan Advisors based in Dallas.

John Alvarez has been a cornerstone of the retirement plan services industry since 2008. With a career that spans both the wholesale and retail sides of the business, John brings a unique perspective and a wealth of experience to his role at IMA Retirement. His journey has seen him excel in various capacities, from leading the retirement plan services practice at Family Wealth Advisers to consulting with Austin Capital Trust Company and driving sales at RetireBetter.

But beyond his impressive professional achievements, John is a person of many passions and inspirations. His favorite novel, Lonesome Dove by Larry McMurtry, speaks to his appreciation for complex characters and relatable life themes. This love for storytelling and depth is mirrored in his approach to helping clients design optimal retirement plans, where every detail matters.

Travel is another of John’s great loves, with Mexico holding a special place in his heart. The vibrant culture, delectable cuisine, and stunning natural beauty of its beach locations offer him a perfect escape and a chance to practice his Spanish. This appreciation for diverse experiences enriches his interactions with clients, bringing a touch of global perspective to his work.

John’s inspiration comes from a deeply personal place—his father. Describing his dad as his hero, John strives to live by the values of kindness, thoughtfulness, and family devotion that his father embodied. This personal ethos translates into his professional life, where he aims to provide the same level of care and dedication to his clients.

When it comes to food, John is a connoisseur of traditional Mexican cuisine, admiring its complexity and historical influences. Yet, he also finds joy in the simplicity of Tex-Mex cheese enchiladas. Cooking is more than a hobby for John; it’s a way to unwind and create something special for his family. The process of planning and preparing a unique meal is a source of satisfaction and relaxation for him.

One piece of advice that has profoundly impacted John comes from his wife: “Don’t tell me what you are going to do. Show me.” This mantra resonates deeply with him, especially in his role at IMA Retirement, where delivering tangible results to clients is paramount.

John’s favorite season is College Football season, a time filled with the excitement of games and the crispness of fall weather. A proud supporter of the Texas Longhorns, he eagerly anticipates the drama and thrill of each game. If he could instantly acquire a new skill, it would be playing the guitar, envisioning the therapeutic and relaxing experience of strumming away on a quiet evening.

Mornings for John start with a cherished routine: a quiet cup of coffee while catching up on news or reading a book. This peaceful start to the day allows him to gather his thoughts before diving into the busyness of work and family life.

John Alvarez’s dedication to his clients, his passion for his work, and his rich personal life make him an invaluable member of the IMA Retirement team. We’re proud to have him with us and look forward to his continued contributions.

For assistance with your retirement needs, contact an IMA Retirement advisor

at retirement@imacorp.com or call 877.305.1864.